The Revenue Reality Check: What Andreessen Horowitz's AI Spending Report Reveals About Who's Actually Monetizing Intelligence

In the gold rush of artificial intelligence, traffic is easy to measure—but revenue is hard to earn. For years, the AI industry has been evaluated by engagement metrics: daily active users, session length, viral coefficients. These are useful indicators of interest, but they do not answer the fundamental question of sustainability: who is actually getting paid? Now, Andreessen Horowitz has published a landmark study that cuts through the noise. By analyzing transaction patterns among the 200,000+ clients of finance startup Mercury, the a16z AI Spending Report reveals which AI companies are converting curiosity into cash flow. This isn't a popularity contest; it is a financial audit of the AI economy. And the results offer a clear-eyed view of where value is being created—and captured.

Methodology Matters: Transactions Over Traffic

The report's approach is its greatest strength. Rather than relying on self-reported usage or third-party web analytics, a16z examined actual spending data from Mercury's business customer base. This provides a direct window into enterprise and professional adoption: when a company pays for an AI tool, it signals that the tool delivers measurable value. The methodology filters out vanity metrics and focuses on economic validation. For investors, founders, and enterprise buyers, this shift from "how many people use it" to "how many people pay for it" is a critical maturation of the market.

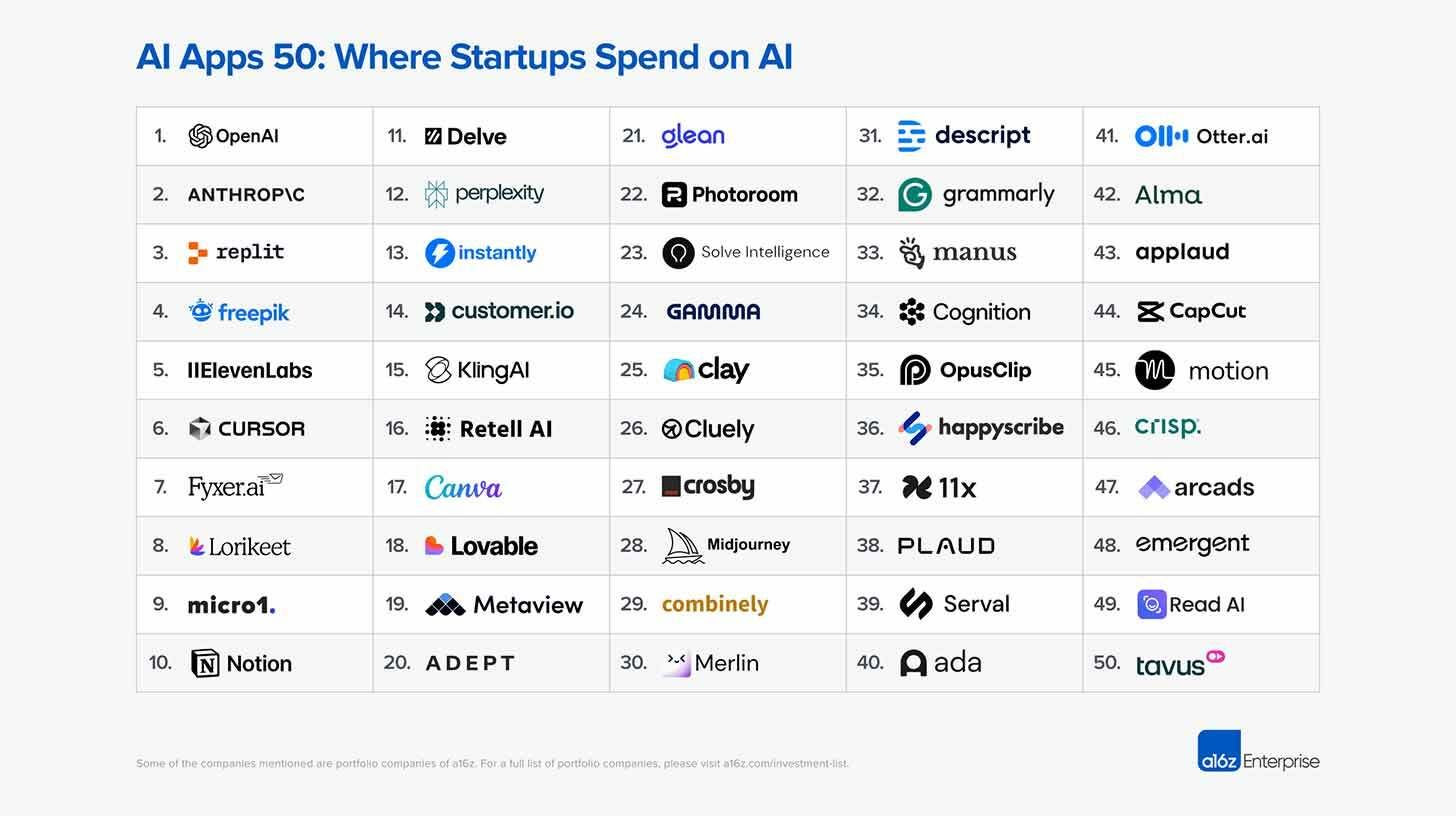

The Rankings: Who's Winning the Monetization Race?

General Assistants: The Duopoly at the Top

Unsurprisingly, OpenAI claims the #1 spot, with Anthropic at #2. This reflects the entrenched position of ChatGPT and Claude as the default interfaces for conversational AI. What is more notable is the presence of Perplexity at #12 and Merlin AI at #30—specialized assistants that have carved out niches by offering distinct value propositions (research-focused answers for Perplexity, productivity integration for Merlin). The long tail of general assistants suggests that while the category is dominated by leaders, there is room for differentiated players to capture meaningful revenue.

Creative Tools: The Largest and Most Diverse Category

With ten companies featured, creative tools represent the most vibrant monetization segment. The rankings reveal a mix of established players and AI-native innovators:

Freepik (#4) and Canva (#17): Traditional design platforms that have successfully integrated AI to enhance their core offerings

ElevenLabs (#5): A pure-play AI voice synthesis company that has found strong enterprise demand

Kling (#15): An emerging video generation tool gaining traction among professional creators

This diversity indicates that creative professionals are willing to pay for AI tools that directly enhance their workflow—whether through speed, quality, or new capabilities. The category's size also suggests that visual and audio content creation is where AI's value proposition is most immediately tangible.

Vibe Coding: From Personal Productivity to Professional Infrastructure

Four "vibe coding" platforms made the list: Replicate, Cursor, Lovable, and Emergent. This is a significant signal. Vibe coding—using natural language to generate, edit, or debug code—was initially framed as a tool for individual developers experimenting with AI. Its presence in enterprise spending data indicates that these tools are scaling into professional workflows. Developers are not just playing with AI; they are relying on it to ship production code. This shift from novelty to necessity is a critical inflection point for the category.

Emerging Categories: Agentic AI, Meeting Assistants, and Vertical Workers

The report highlights several other growing segments:

Meeting assistants: Tools that transcribe, summarize, and actionize conversations are gaining enterprise adoption

AI workers for specific activities/industries: Specialized agents for sales, support, legal, or healthcare are moving beyond pilots into paid deployment

Agentic tools: Platforms that enable autonomous, multi-step workflows are beginning to show monetization traction

These categories represent the next wave of AI value: not just generating content, but executing tasks. The fact that they appear in spending data suggests that enterprises are willing to pay for automation that delivers measurable efficiency gains.

Strategic Implications: What the Data Tells Us About AI Monetization

1. Integration Beats Isolation

The companies that rank highest tend to embed AI into existing workflows rather than requiring users to adopt entirely new paradigms. Canva didn't replace design; it augmented it. Cursor didn't replace IDEs; it enhanced them. This pattern suggests that the most sustainable AI businesses are those that reduce friction, not those that demand behavioral change.

2. Specialization Commands Premiums

While general assistants dominate by volume, specialized tools often achieve higher revenue per user. ElevenLabs (voice), Freepik (design assets), and Perplexity (research) have found willing buyers by solving specific problems exceptionally well. This indicates that niche dominance can be as valuable as broad adoption.

3. Enterprise Adoption Is Accelerating

The Mercury dataset reflects business spending, not consumer subscriptions. The presence of diverse AI categories in this data signals that enterprises are moving beyond experimentation into scaled deployment. This is a critical inflection point: when AI shifts from IT pilot to departmental budget, revenue becomes more predictable and durable.

4. The "Vibe Coding" Evolution Is Real

The inclusion of four coding-focused platforms in enterprise spending data validates a hypothesis: AI-assisted development is transitioning from a personal productivity hack to a professional infrastructure layer. As these tools demonstrate ROI through faster shipping, fewer bugs, or reduced onboarding time, adoption will accelerate.

The Bigger Picture: From Hype to Economics

The a16z report does more than rank companies; it reframes how we evaluate AI progress. For too long, the industry has celebrated model capabilities, benchmark scores, and user growth—metrics that matter, but do not guarantee sustainability. By focusing on actual spending, the report forces a more disciplined conversation: What problems are customers willing to pay to solve? Which AI capabilities translate into economic value? How do business models evolve as the technology matures?

This shift is healthy. It encourages founders to build for revenue, not just engagement. It helps investors allocate capital to businesses with viable economics. It guides enterprises toward tools that deliver measurable ROI. And it reminds the broader ecosystem that AI is not just a technological phenomenon—it is an economic one.

Risks and Considerations: Spending Data Is Not Destiny

While the report provides valuable insights, it is important to acknowledge its limitations:

Sample bias: Mercury's client base may overrepresent tech-forward startups and underrepresent traditional enterprises

Timing: Spending patterns reflect current adoption; they do not predict future winners

Category definitions: Labels like "vibe coding" or "agentic tools" are evolving and may not capture the full landscape

Revenue vs. profit: Spending indicates top-line traction, but not necessarily sustainable unit economics

These caveats do not diminish the report's value; they contextualize it. The goal is not to declare permanent winners, but to identify trends that warrant attention.

Forward-Looking Insights: Where to Watch Next

Based on the report's findings, several areas deserve close observation:

Agentic AI monetization: As autonomous workflows move from demo to deployment, which pricing models will emerge? Per-task, per-outcome, or subscription?

Vertical AI consolidation: Will specialized tools for healthcare, legal, or finance remain fragmented, or will platforms emerge that unify multiple use cases?

Open-source vs. proprietary: How will monetization strategies evolve as open-source models improve and reduce dependence on proprietary APIs?

International expansion: The report reflects U.S.-centric spending; how will AI monetization patterns differ in Europe, Asia, or emerging markets?

Conclusion: The Monetization Mandate

Andreessen Horowitz's AI Spending Report is more than a ranking; it is a reality check. It reminds us that in the end, technology must create economic value to endure. The companies that thrive will not just be those with the most impressive demos, but those with the clearest path to revenue.

For founders, the message is clear: build for value, not just virality. For investors, the lesson is to prioritize unit economics over user growth. For enterprises, the takeaway is to evaluate AI tools by their impact on outcomes, not just their novelty.

The AI gold rush is real. But as in any gold rush, the lasting fortunes will belong not to those who dig the fastest, but to those who build the most sustainable operations. The a16z report provides a map. The question is: who will use it to build something that lasts?

The era of AI as a curiosity is ending. The era of AI as a business is here. The spending data proves it. Now, the work begins.

Your one-stop shop for automation insights and news on artificial intelligence is EngineAi.

Did you like this article? Check out more of our knowledgeable resources:

Watch this space for weekly updates on digital transformation, process automation, and machine learning. Let us assist you in bringing the future into your company right now